Is your RRSP ready for you to retire?

Article Licenses: CA, DL, unknown, unknown, unknown

Advisor Licenses:

Compliant content provided by Adviceon® Media for educational purposes only.

The Canadian government regulates the Registered Retirement Savings Plan (RRSP) program, allowing it to have unique tax benefits as you save for your retirement. Annual RRSP contributions can reduce the amount of income tax you pay in the year of your contribution. These monies invested annually grow on a tax-deferred basis, and tax is only paid at the time of withdrawal. RRSP Planning is a very integral part of your investment planning.

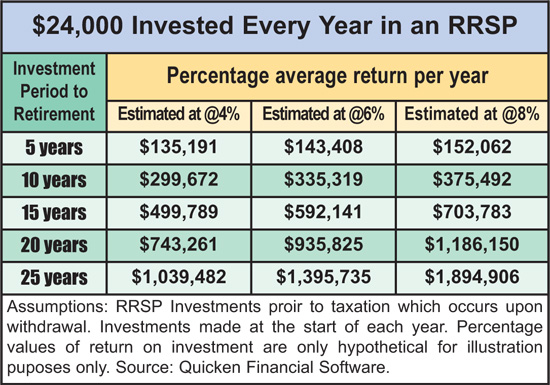

Have a look at the graph below to see how RRSP money accumulates over time based on a maximum annual investment.

Your investments grow tax-free Your RRSP investments accumulate within the plan tax-free, as do any addition to your contributions, including capital gains, interest, dividends, and any other growth via dividends or distributions paid out on an investment fund. The longer your money stays sheltered from the taxman, the greater the tax-free accumulative earning power of your investment. However, taxation occurs once income is withdrawn from your RRSP.

Planning Together – Spousal RRSPs and Tax

A spousal RRSP allows a couple to place assets in the lower-earning spouse’s registered account. The benefit of this manoeuvre enables the account owner to withdraw more in retirement at a lower tax bracket while retaining spousal RRSP ownership, controlling the choice of the RRSP investment vehicles. The owner also governs when withdrawals are made and pays the income taxes upon withdrawal (if the funds have been in the account for three years).

What happens when the RRSP account holder dies?

For estate planning purposes, upon the decease of the account holder, the RRSP is paid out to the beneficiary designated for that account.

How Much can you contribute to your RRSP?

Your Contribution Limit To find out your allowable RRSP contributions you are allowed to deduct for your income taxes, check Last Year’s Deduction Limit Statement on your latest Notice of Assessment or Notice of Reassessment. Canada Revenue Agency (CRA) establishes guidelines for the minimum and maximum overall yearly amount a person is eligible to contribute to their RRSP. The basic formula used to determine a taxpayer’s eligible contribution is as follows: 18% of earned income minus any Pension Adjustment = the eligible contribution amount.

Who can contribute to an RRSP? All Canadian taxpayers with “earned income” in the previous tax year, or those having unused contributions carried forward from previous years can contribute to their RRSP. A person is eligible to make contributions to their RRSP until December 31 in the year they reach age 71, provided that they have contribution room.

Two methods of contributing to your RRSP You may invest by purchasing a lump sum investment prior to the deadline. The alternative is to invest on a monthly basis using dollar-cost averaging. You can always top up your RRSP contribution (up to the allowable limit), just prior to the deadline year by year.

The RRSP limit Table

Source: CRA

Revised: January 2021

Publisher's Copyright & Legal Use Disclaimer

All articles are a legal copyright of Adviceon®Media and are for educational

purposes only. The particulars contained herein were obtained from sources

which we believe are reliable, but are not guaranteed by us and may be

incomplete. This website is not deemed to be used as a solicitation in a

jurisdiction where this representative is not registered. This content is not

intended to provide specific personalized advice, including, without

limitation, investment, insurance, financial, legal, accounting or tax

advice; and any reference to facts and data provided are from various sources

believed to be reliable, but we cannot guarantee they are complete or

accurate; and it is intended primarily for Canadian residents only, and the

information contained herein is subject to change without notice.

References in this website to third party goods or services should not be

regarded as an endorsement, offer or solicitation of these or any goods or

services. Always consult an appropriate professional regarding your particular

circumstances before making any financial decision. The information provided

is general in nature and should not be relied upon as a substitute for advice

in any specific situation. The publisher does not guarantee the accuracy and

will not be held liable in any way for any error, or omission, or any

financial decision.

Mutual Funds Disclaimer

Commissions, trailing commissions, management fees and expenses all may be

associated with mutual fund investment funds, including segregated fund

investments. Please read the fund summary information folder prospectus

before investing. Mutual Funds and/or Segregated Funds may not be

guaranteed, their market value changes daily and past performance is not

indicative of future results. The publisher does not guarantee the accuracy

and will not be held liable in any way for any error, or omission, or any

financial decision. Talk to your advisor before making any financial

decision. A description of the key features of the applicable individual

variable annuity contract or segregated fund is contained in the Information

Folder. Any amount that is allocated to a segregated fund is invested at the

risk of the contract holder and may increase or decrease in value. Product

features are subject to change.

Life Insurance and Segregated Funds Disclaimer

Life Insurance policies vary according to contract terms. Please read any

Life Insurance policy contract provided, or the segregated fund summary

information folder prospectus before the time of purchase. Full details of

coverage, including limitations and exclusions that apply, are set out in

the policy of insurance. Commissions, trailing commissions, management fees

and expenses may be associated with segregated fund investments which may

not be guaranteed and their market value changes daily and past performance

is not indicative of future results. A description of the key features of a

life insurance policy, a segregated fund; and any applicable individual

variable annuity contract is contained in information provided by the

company from which it is purchased. Talk to your advisor before making any

financial decision. For specific situations, advice should be obtained from

the appropriate legal, accounting, tax or other professional advisors. The

information provided is accurate to the best of our knowledge as of the date

of publication and is general in nature, intended for educational purposes

only, and should not be relied upon as a substitute for advice in any

specific situation. For specific situations, advice should be obtained from

the appropriate legal, accounting, tax or other professional advisors.

Rules and their interpretation may change, affecting the accuracy of the

information.